The world’s biggest banks reportedly slashed more than 60,000 jobs in 2023.

It was a year in which investment banks suffered their second year in a row of declining fees amid a downturn in dealmaking and companies going public, the Financial Times (FT) reported Monday (Dec. 25).

In addition, the report said, UBS’ takeover of Credit Suisse has led to at least 13,000 fewer roles at the combined bank, with another round of layoffs expected in 2024.

“There is no stability, no investment, no growth in most banks — and there are likely to be more job cuts,” Lee Thacker, owner of financial services headhunting company Silvermine Partners, told the FT, adding, “There are some very nice gifts being sent to bosses at the moment.”

According to the FT’s calculations, 20 of the world’s largest lenders cut at least 61,905 jobs this year. It was one of the worst years for job cuts at banks since the 2007-2008 financial crisis, when banks eliminated 140,000 positions.

Aside from UBS, the second largest number of job cuts happened at Wells Fargo, which reduced its headcount by 12,000.

The bank will also likely see greater-than-expected expenses from severances tied to those job cuts, with the price tag for those layoffs expected to reach $750 million to just shy of $1 billion for the banking giant’s fourth quarter, CEO Charlie Scharf said earlier this month.

“We are continuing to focus on efficiency with turnover dropping, unfortunately, we’re going to have to be more aggressive about our own internal actions,” Scharf said.

In total, the big Wall Street banks cut at least 30,000 jobs this year: 5,000 at Citi, 4,800 at Morgan Stanley, 4,000 at Bank of America, 3,200 at Goldman Sachs 3,200 and 1,000 at JPMorgan Chase.

“The revenues aren’t there, so this is partly a response to overexpansion. But there is also a simpler explanation: political cost-cutting,” Thacker said. “If you run a division and your boss asks for savings, you cut or you get fired.”

It’s not just banks cutting jobs amid a tougher economic climate. This year saw more than 250,000 tech workers lose their jobs, as both massive companies like Google and tiny startups cut their workforces.

Emerging Market FinTechs Poised to Drive Innovation and Inclusion in 2024

In 2023, the FinTech landscape experienced a transformative surge of innovations, reshaping financial technology from its core. These advancements, spanning cutting-edge technologies and the evolution of business models, have ignited a pivotal shift that goes beyond mere functionality, altering how financial services are accessed and utilized.

In a recent interview with PYMNTS, Jori Pearsall, chief business officer at Tala, discussed this wave of innovation, particularly highlighting its resonance in emerging markets like Southeast Asia. He pointed to the recent milestone of digital payments surpassing 50% of transactions in the region, signaling a departure from cash dominance.

This shift, he said, presents a promising opportunity for FinTech firms, which can leverage the burgeoning mobile adoption trend to unlock access to a vast audience in the upcoming year.

Pearsall also highlighted the digital lending gap in Mexico — it stands at a mere 18% against an 80% mobile penetration rate — as another significant growth potential for FinTech companies to leapfrog into mobile-based financial services, a trend mirrored across Latin American countries.

India, another market brimming with potential, has made remarkable strides in digital infrastructure, Pearsall said, citing initiatives like the Unified Payments Interface (UPI) as a driving force behind the ubiquity of digital transactions in the country.

However, despite high bank account penetration, nearly 80% of India’s population remains financially underserved, presenting a compelling landscape for FinTech players to bridge the gap. “When you have this kind of melting pot of strong technical solutions and a large, underserved audience, you’ll see a lot of tech-savvy players trying to dive in in the year to come to close that gap,” Pearsall said.

Bank-FinTech Collaborations

Acknowledging the challenging macro environment going into 2024, Pearsall emphasized a shift toward more partnerships between FinTech startups and established incumbents, with both sides leveraging their strengths for mutual benefit.

For FinTech firms increasingly focusing on belt-tightening amid mounting pressure from investors to pivot from growth to profitability, Pearson’s view is that collaborations with incumbents will become increasingly critical, not just in sustaining business models but also in enhancing customer value propositions.

“We have FinTechs that are more nimble, flexible and can bring solutions to market more quickly, but at the same time, gone are the days of abundant cheap venture capital dollars,” Pearsall said.

On the other hand, a tighter macro climate generally translates to more constrained budgets for incumbents’ in-house teams, which in turn puts internal research and development (R&D) on the back burner. In this scenario, partnerships with FinTechs will become the avenue to foster innovation, he said, adding that this mutual recognition will drive both established incumbents and burgeoning FinTechs toward a shared pursuit of collaborative initiatives.

Despite having built a robust in-house solution for its services, Tala, too, recognizes the value in these partnerships, Pearsall said. In fact, these collaborations remain pivotal to the firm’s growth, enabling access to new audience segments and facilitating the swift and cost-effective expansion of service offerings for end consumers.

As he noted: “When there’s this pressure toward partnerships, ultimately the customer value proposition should get stronger. And when the customer value proposition gets stronger, good things tend to happen.”

AI and ML Transform Lending

Artificial Intelligence (AI) and machine learning (ML) have emerged as game-changers in the FinTech landscape, and particularly in the emerging market lending space, Pearson said, echoing similar insights shared by Tala Chief Technology and Product Officer Kelly Uphoff in a separate PYMNTS interview.

Across these markets, the complexities of providing real-time, personalized decision-making across diverse languages and cultures pose considerable challenges, especially given the limited data available and often minimal or even nonexistent formal credit histories.

“Sometimes, there’s not even much of an identity history, [however], with the latest advancements in AI and ML, [lending] is getting better, faster, easier,” he said. Pointing to AI-driven platforms like Metaflow, he said these tools have transformed the underwriting process, enabling the swift delivery of personalized decisions in near real time.

Beyond lending, Pearsall said AI and ML advancements promise elevated customer service experiences in the coming year, enabling faster and more personalized responses, which will be critical in catering to millions of emerging markets “coming online and accessing these services digitally for the first time.”

Overall, as 2024 unfolds, the FinTech space is bracing for accelerated advancements, driven by collaborative endeavors, evolving regulations, and AI-powered innovations. These driving forces are set to usher in progressive changes for millions of underserved populations, while opening new avenues for inclusive access across the global financial landscape.

Mobile Helps Brand Loyalty Programs Work Harder and Smarter

Technology, and the digital transformation of the economy overall, have reshaped the concept of customer loyalty.

Add to that the integration of payments innovation, and the loyalty program ecosystem of today is nearly unrecognizable compared to years past.

“The phone has been the cohesive unit that pulls all [this technical innovation] together,” Len Covello, chief technology officer at Engage People, told PYMNTS. “We’ve been hearing the term omnichannel for probably 10-plus years, but we’ve gotten there with the device itself and integrating payments into one-click checkouts and more.”

The smartphone has become the central device that people use to interact socially, at home, on the go and even in stores.

And with ongoing advancements in mobile device technology and payments innovation, loyalty programs have the potential to become even more effective in driving customer retention and reinforcing personal relationships while building lifetime value.

The integration of payments into the smartphone has also played a significant role in enhancing loyalty programs, Covello explained. With a simple click on a phone, customers can now make seamless payments, eliminating the need to wait in queues. They can even pay with their loyalty points or receive personalized offers while making a purchase.

This level of convenience and personalization creates a perfect ecosystem for loyalty transactions.

“We’ve got all the tools available today,” Covello said.

Enhancing Loyalty With Tech and Payments

Loyalty programs have long been a staple in the business world, offering rewards and incentives to customers who repeatedly engage with a brand.

Many brands have already started leveraging digital wallets and contactless payments to enhance the delivery of their loyalty programs.

Starbucks, Covello noted, has successfully implemented this approach. By controlling the entire environment and integrating its loyalty program with its payment terminals, Starbucks has created a seamless and rewarding experience for its customers. Other retailers and brands are following suit, using the data gathered from smartphones to understand customer behaviors and provide personalized offers.

“That device knows a lot about you, and really when we talk about loyalty, that interaction with the loyalty program is about gathering data on the user and gathering behaviors,” he added.

The concept of an ecosystem is crucial in this context. As customers interact with different devices throughout their day, such as smartphones, virtual assistants or even smart vacuums, each device collects data about their preferences and behaviors.

By unifying logins across devices, brands can track customers’ activities and deliver targeted ads and offers. Covello acknowledged that while there may be concerns about privacy, loyalty programs have always been based on the exchange of data for personalized benefits. When done well, this data-driven approach can bring tremendous value to consumers.

Accelerating the Loyalty Partnership

Within this data-rich context, artificial intelligence (AI) and machine learning are becoming instrumental in making sense of the vast amount of data collected by loyalty programs.

By analyzing customer data, AI can identify meaningful patterns and preferences, allowing brands to deliver offers that align with customers’ needs and budgets. Covello pointed out that during the pandemic, loyalty programs focused on providing offers for essential items like gas and groceries, considering the economic uncertainties faced by consumers.

“The advancements of machine learning and AI will help us crunch that data and bring better personalized offers,” he said. “And the more devices we interact with, the more personalized that offer will be.”

Gamification is another aspect that can enhance loyalty programs. By turning the loyalty journey into a game-like experience, brands can make it more engaging and rewarding for customers, Covello said, noting that “rewarding and gamification are essentially one and the same.”

Rewards can take various forms, including points, tiers or exclusive access to limited availability items. Industries that have limited availability, such as shoe companies releasing new products, can particularly benefit from gamifying their loyalty programs, Covello said.

As for what he sees 2024 holding?

“The partnership aspect of things will continue to accelerate,” Covello said, explaining that brands with similar values and target customers will collaborate to offer a more comprehensive loyalty ecosystems.

In an environment where consumers are tightening their belts, brands that can bring value and meaningful partnerships will be successful, he added.

Smart Credit Card Use Turns Debt Burdens Into Financial Flywheels

The holidays can be a stressful time financially for many consumers.

Often, those consumers — particularly those living paycheck to paycheck — turn to their credit cards as an essential financing tool. But these quick-fix expenditures can add up.

“Americans now owe over $1 trillion in, in credit card debt. Credit card balances and interest rates are the highest that they’ve been,” Amber Carroll, senior vice president of membership and lifecycle at LendingClub, told PYMNTS in a conversation unpacking findings from the “New Reality Check: The Paycheck-to-Paycheck Report,” a PYMNTS Intelligence collaboration with LendingClub that explores how consumers are using credit as inflation continues.

Within today’s challenging environment it is crucial to understand how consumers are utilizing credit cards and the impact it has on their financial well-being.

“More than half of credit cards are held by consumers who are living paycheck to paycheck,” said Carroll, noting that credit cards are being used by this consumer cohort primarily as a financing tool rather than solely for convenience.

Paycheck-to-paycheck consumers prioritize credit lines, rates and fees when selecting credit cards. They are more likely to utilize flexible repayment options and view credit as a means to manage their finances.

On the other hand, Carroll said, consumers who are not living paycheck to paycheck focus more on rewards and may not take advantage of flexible repayment programs as frequently.

“It will be really important to look at what happens with interest rates over the months ahead. An interest rate cut could mean lower monthly payments. And that’s a trend that will certainly help those who are living paycheck to paycheck and using the revolving capabilities on credit cards,” she added.

The Growing Reliance on Credit Cards as a Means to Get By

Despite the challenges associated with credit card debt, the demand for credit cards is expected to remain strong.

“It’s a positive sign to see that even half of consumers living paycheck to paycheck are maintaining high credit scores. This shows that despite a tighter economic lifestyle, they are still prioritizing good credit behavior,” Carroll said.

“The challenge based on the data we see is managing credit utilization. Credit cards can keep many in debt and it’s very easy for that debt to snowball into more debt or longer running revolving debt,” she said, noting that 43% of all cardholders have had a revolving balance on their credit cards at least occasionally in 2023. And that number has increased from 41% in 2022.

That’s why it is essential for consumers to use credit as a tool rather than a crutch. Paying for urgent purchases in full and keeping credit balances below 30% of available credit are recommended strategies to maintain a healthy credit score.

Carroll points out the fact that many consumers say they used debit cards for their last purchase, indicating that paycheck-to-paycheck consumers are trying to live within their means and avoid overextending themselves on credit cards.

However, credit card usage for financing needs is still prevalent, and it is unlikely to change in the near future.

Carroll noted that close to one-third of consumers say they have reached their credit limit, which is an average of $9,200, at least occasionally in the last year, and that amount more than doubles to about 64% for those who are having a hard time paying bills.

Keys to Improving Overall Financial Health for Consumers

For paycheck-to-paycheck consumers looking to improve their credit scores, a combination of financial education, budgeting tools and credit building strategies is essential, Carroll said.

Actively monitoring credit reports, practicing good credit behavior, avoiding overextension and keeping old credit card lines open can all contribute to improving credit scores and overall financial health.

“Having a diverse mix of credit is a great way to show well-rounded responsible credit usage, but avoid applying for too much new credit in a short amount of time as that can appear like you’re desperate for credit,” says Carroll.

“We’re seeing a lot of high credit usage right now. I think looking ahead, hopefully we will be getting some macro relief around interest rates so that folks can start to pay down those balances and get them into reasonable ranges,” she said.

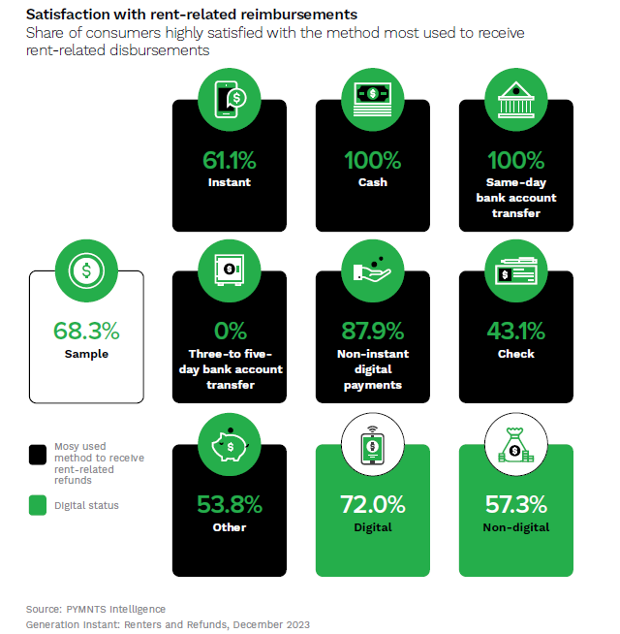

Nearly Two-Thirds of Renters Highly Satisfied With Receiving Refunds Instantly

Just as digital options have gained popularity for paying rent directly from a bank account, the digitization of refunds has also gained momentum. In fact, the days of writing checks and mailing them are dwindling, with tenants, particularly those with higher rents, increasingly favoring convenient, hassle-free digital and instant transactions.

“Generation Instant: Renters and Refunds,” a PYMNTS Intelligence and Ingo Money collaboration, draws insights from a survey of more than 2,600 consumers across the United States to examine consumer satisfaction with rent-related disbursements received from government and non-government entities.

According to findings detailed in the study, renters favor receiving instant refunds to their bank accounts over digital wallets and cards. In fact, among those who received rent-related refunds, 40% primarily used instant methods, with 19% receiving most of those payments instantly to a bank account and 13% to a digital wallet.

The data also shows that rent-related refunds received via instant payments are, on average, 46% larger than those received via non-instant methods. This suggests that when receiving higher rent-related refunds, tenants prefer to receive them sooner rather than later. Additionally, the average refund received via an instant method is higher than non-instant methods, indicating the value renters place on receiving larger refunds promptly.

Examining the data further shows that while only 57% of renters receiving refunds via non-digital payment methods report high satisfaction, a significant 72% of renters receiving refunds via digital payment methods express high satisfaction. Furthermore, 61% of renters express immense satisfaction with receiving rent-related refunds via instant payment methods, indicating that property management companies offering digital and instant refund options have a competitive advantage in attracting tenants.

It is worth noting, however, that 44% of renters were not offered the option to receive instant payments, and 35% of this group would have chosen instant payments if given the choice. This highlights the potential for property management companies to improve refund satisfaction by meeting the demand for instant payment methods.

That said, not all renters are keen on embracing faster payments. Among those who do not prefer to receive rent-related refunds via instant payment methods, security concerns and a reluctance to share payment credentials were the top reasons. Additionally, a lack of incentives and rewards for using instant payments was a common deterrent. However, cost was not a significant factor for most renters, indicating their willingness to pay for instant access to their funds.

In summary, the shift toward faster rent-related refunds is evident, with renters clearly indicating their preference for receiving refunds digitally and instantly. Property management companies have a golden opportunity to engage and attract high-income, digitally savvy consumers by offering these payment options, while addressing security concerns and providing incentives that align with modern consumer expectations.

Zulily’s Last Checkout: The Retail Road to Its Online Closure

Online retailer Zulily is calling it quits.

In the latest update from PYMNTS regarding Zulily, once navigating the choppy waters of a fiercely competitive sea, has disclosed its intentions of undergoing a liquidation process.

In fact, just seven months into its tenure under new ownership, the Seattle-based online retailer is in the process of winding down its operations.

As of Friday (Dec. 22), the online retailer has officially halted its operations. The company shared in a statement on its no-longer-active website that it has begun a process called an assignment for the benefit of creditors (ABC). Instead of going through bankruptcy, this involves selling off Zulily’s assets in the next 12 to 18 months.

“This decision was not easy nor was it entered into lightly,” said Ryan Baker, vice president of Douglas Wilson Companies in a statement. “However, given the challenging business environment in which Zulily operated, and the corresponding financial instability, Zulily decided to take immediate and swift action.”

The confirmation that Zulily has ceased operations marked the initial public acknowledgment of the company’s status. Before this, there was uncertainty about whether the company was in the process of closing down or had already completed its operations. The announcement on Friday came after the website suddenly went offline about a week earlier, showing a blank page with a “We are down for maintenance” message. This message appeared after a short period during which Zulily’s homepage had phrases like “final sale” and “all items must go.”

Regent and Baker, the parent company of Zulily, didn’t share additional information about the retailer’s financial situation. There was no immediate response from either party when asked for comments.

Prior to the acquisition, Zulily had experienced financial challenges, particularly in its final year as part of Qurate’s brand portfolio. Zulily reported a 17% decline in revenue in the first quarter, dropping from $232 million to $192 million year over year (YoY), accompanied by a $43 million operating loss for the same period.

Events Prior to Zulily Shutdown

Earlier this month, revelations surfaced following mandatory notices submitted to state employment authorities, indicating that Zulily intended to terminate over 800 employees in Washington, Nevada, and Ohio.

Shortly after the announcement of these widespread layoffs, Zulily took legal action against Amazon, alleging the eCommerce giant participated in price fixing and pressured third-party sellers and wholesale suppliers to artificially increase prices on Zulily. The lawsuit contended that Amazon had “abused its monopoly power,” hindering Zulily’s ability to compete in the online retail space. Amazon, however, denies any wrongdoing.

In May, Regent acquired Zulily from Qurate Retail, the parent company of QVC and HSN, for an undisclosed amount.

In the latter part of 2022, PYMNTS highlighted that Qurate Retail was encountering challenges while dealing with surplus inventory in the eCommerce market post-pandemic.

In a press release, President and CEO David Rawlinson II mentioned that the third quarter 2022 earnings results of the company revealed a highly competitive promotional landscape and diminished consumer sentiment.

During that period, Qurate’s revenue fell 13%, amounting to $2.7 billion, and its eCommerce revenue also fell 13%, reaching $1.7 billion.

In the same time frame, QVC International revenue fell 21%, QxH revenue dropped 8%, and Zulily’s declined 39%. On the positive side, another retail brand under the Qurate umbrella, Cornerstone, managed to increase revenue by 8%.

The company had also announced in the release that it was restructuring its presence in Europe. In fact, Qurate had entered into an agreement for the sale and leaseback of its United Kingdom and Germany fulfillment centers for about £68 million (about $77 million) and €97 million (about $96 million), respectively. The company had planned to close this deal in the first quarter of 2023.

Qurate faced similar issues in the last quarter, with the company’s revenue decreasing by 16% at that time.

However, as the company headed into the fourth quarter, sentiment surrounding two quarters of weak earnings results led Qurate to reevaluate its strategy.

Decreased Consumer Sentiment

Late last year, retailers were eager to encourage consumers fatigued by inflation to spend more. They intensified promotions, grappling with the challenge of clearing out excess inventory that had already been marked down.

The abundance of deals was a sharp departure from the year prior. In fact, two holiday seasons ago, shoppers had started buying gifts early to avoid out-of-stock and shipping delays. Concerns about not getting hot items had meant consumers were willing to pay up.

Then in 2022, retailers found themselves with a surplus of merchandise as consumers said inflation was twice as bad as the government actually reported.

Read more: Consumers Say Inflation Twice as Bad as Government Reports

Shoppers were hesitant to spend due to increased costs in areas such as food, housing, healthcare, and other essential items, with inflation reaching levels not seen in four decades. Additionally, people were allocating more of their money to travel and experiences following over two years of COVID-related restrictions.

Central Bank of Nigeria Lifts Ban on Transacting in Crypto

The Central Bank of Nigeria (CBN) has lifted a ban on transacting in cryptocurrencies.

At the same time, the bank said there is a need to regulate virtual asset service providers (VASPs), including cryptocurrencies and crypto assets, Reuters reported Wednesday (Dec. 27), citing a Friday (Dec. 22) circular issued by the bank.

The CBN imposed a ban on banks and financial institutions dealing in or facilitating transactions in crypto assets in February 2021 due to concerns over money laundering and terrorism financing, according to the report.

However, the Securities and Exchange Commission, Nigeria published regulations in May last year that aimed to find a middle ground between an outright ban and unregulated use of crypto assets, the report said.

In its circular dated Dec. 22, the CBN outlined guidelines for banks and financial institutions regarding the opening of accounts, designated settlement accounts, settlement services, and acting as channels for foreign exchange inflows and trade for firms transacting in crypto assets, per the report. The guidelines emphasize the need for VASPs to obtain licensing from the Nigerian SEC to engage in crypto business.

The circular also states that banks are still prohibited from trading, holding or transacting cryptocurrencies, according to the report.

Nigeria has witnessed a surge in cryptocurrency adoption, particularly among its young and tech-savvy population, the report said. Many individuals have turned to peer-to-peer trading offered by crypto exchanges as an alternative to traditional financial services.

The volume of crypto transactions in Nigeria grew by 9% year over year to $56.7 billion between July 2022 and June 2023, per the report, which cited data from blockchain research firm Chainalysis.

It was reported in October 2021 that despite the ban from their country’s central bank, people in Nigeria had turned to cryptocurrency to conduct business, send payments and guard their savings.

In November 2022, the Securities and Exchange Commission, Nigeria said that it had no plans to make crypto part of its digital asset trading goals until regulators agree to standards that keep investors safe.

The commission said at the time that it would promote investment in “sensible digital assets,” with investment protection while also looking into blockchain technology to drive virtual and traditional investment products.

Simple Hacking Techniques Prove Successful in 2023 Cyberattacks

Cybercriminals have shown over the past year that sophisticated technology is not always necessary to carry out successful cyberattacks.

Several incidents in 2023 have highlighted the effectiveness of simple hacking techniques in breaching security, Bloomberg reported Wednesday (Dec. 27).

One notable trend is the use of social engineering tactics by hackers, according to the report. The hacking group Scattered Spider employed deceptive phone calls to trick customer service representatives into revealing password credentials. Resorting to aggressive tactics, such as threatening employees with termination, the group managed to breach numerous organizations, including MGM Resorts International, Caesars Entertainment and Coinbase. This straightforward approach has resulted in about 52 breaches since 2022.

Exploiting software with known security flaws has also proven to be an effective low-tech method, the report said. Hackers continued to target companies that failed to promptly update their systems, even after patches were released to fix critical vulnerabilities. Aerospace giant Boeing fell victim to such an attack after Citrix had issued a fix, emphasizing the importance of regular software updates and addressing known security flaws promptly.

The rise in ransomware attacks in 2023 further demonstrated the success of low-tech hacking techniques, per the report. Major firms, banks, hospitals and government agencies experienced a 51% increase in ransomware incidents. These attacks disrupted financial trading, caused shortages of essential products like Clorox wipes, and targeted critical infrastructure. However, due to the lack of transparency surrounding these incidents, reliable figures on the number of data breaches, the extent of the damage and the hackers responsible remain elusive.

Key lessons from post-incident reports include the importance of prioritizing cybersecurity hygiene, regularly reviewing access privileges and conducting thorough business continuity planning, Rosa Ramos-Kwok, managing director and business information security officer for Commercial Banking at J.P. Morgan, and Matanda Doss, executive director and lead information security manager for Commercial Banking at J.P. Morgan, told PYMNTS’ Karen Webster in an interview posted on Thursday (Dec. 21).

“The No. 1 thing that I would start with is good cyber hygiene,” Ramos-Kwok said, explaining that sometimes firms can fall behind on patching up legacy systems, which leaves aged software with “all sorts of vulnerabilities.”

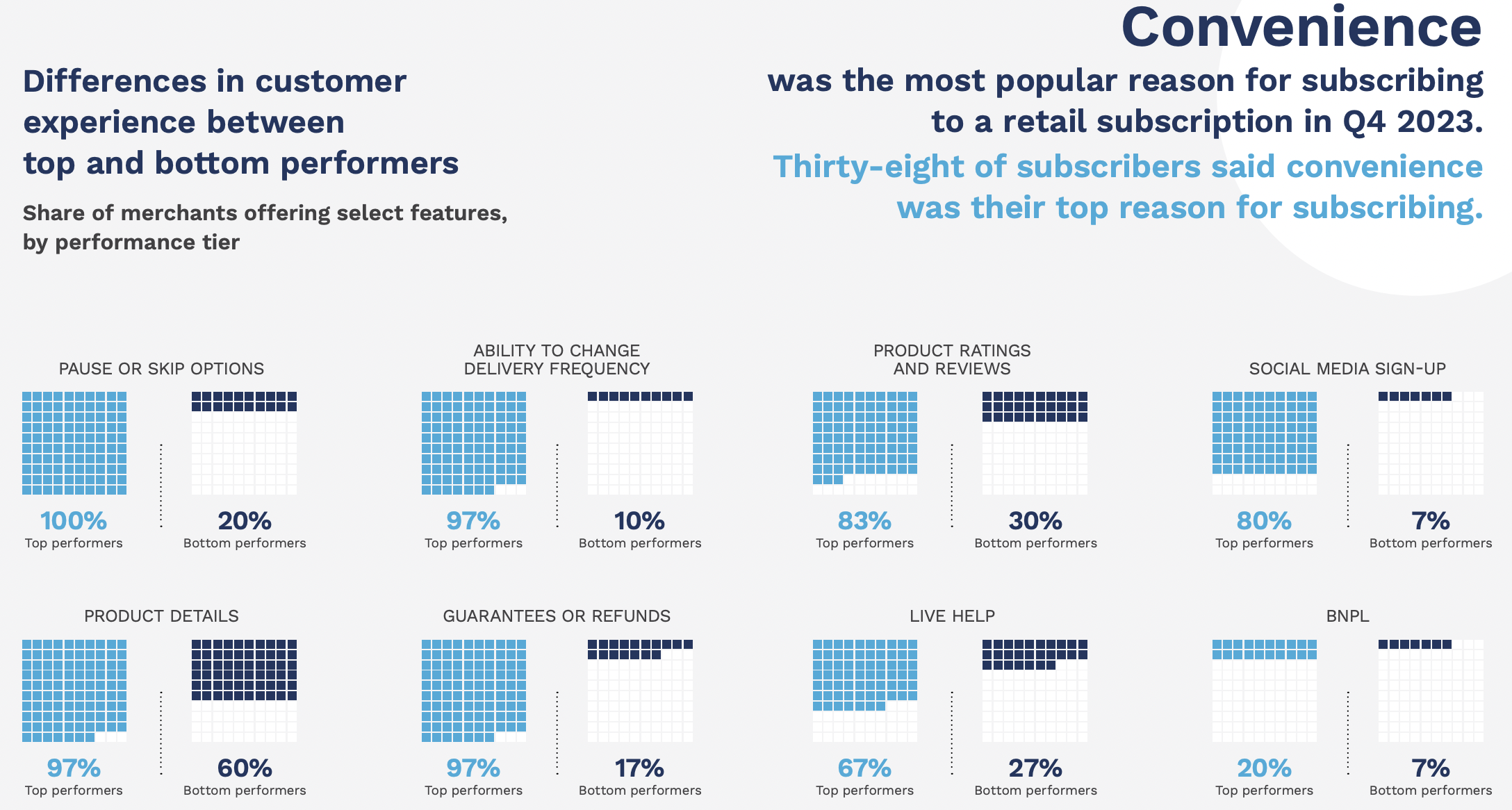

Top-Performing Subscription Merchants Let Their Customers Take a Break

Top-performing retail subscription merchants offer their customers the option to take a step back, while merchants that do not provide this kind of flexibility tend to struggle.

By the Numbers

The December installment of the Decision Guide report, “The Retail Subscription Features That Make Top-Performing Merchants,” a PYMNTS Intelligence and sticky.io collaboration, drew from a survey of 188 retail subscription merchants in September. It examined, among other matters, how various features relate to merchants’ performance.

The results revealed that offering consumers flexible options is strongly linked to subscription providers’ success. For instance, 100% of top-performing merchants offer the option to pause or skip, while only 20% of bottom performers do the same.

A Deeper Dive

Flexible plan options are increasingly becoming table stakes. PYMNTS Intelligence and sticky.io’s study released last month “The Replenish Economy: A Household Supply Deep Dive” revealed that three-quarters of retail subscription merchants allow existing subscribers to change their plans whenever they would like.

Alex Brown, CEO of sustainable cleaning supplies subscription firm Truly Free, noted to PYMNTS’ Karen Webster in a conversation for the series “Tough Questions: Retaining the Selective Subscriber of 2023,” that offering this kind of flexibility is vital to establishing strong relationships with customers.

“Allowing people to see that they can pause or cancel or have this full control over their subscription is what delivered more trust,” Brown said in May. “At the end of the day, it’s about trust.”

In the same conversation, sticky.io CEO Brian Bogosian discussed the different kinds of flexibility that consumers are coming to expect.

“Flexibility is key,” he said. “Flexibility to not only be able to cancel, but to pause, replace products, move to a different tier, as much flexibility as can be provided … extends that customer’s lifetime value.”

From Reservations to Ordering, Gen AI Took Over Restaurants in 2023

In 2023, generative artificial intelligence began to make its way into many different parts of the restaurant industry, across the back- and front-of-house, boosting efficiency and effectiveness.

Earlier this month, for instance, McDonald’s announced a partnership with Google Cloud, through which the quick-service restaurant giant aims to leverage the latter’s generative AI and cloud technology to make operations more efficient and to improve the customer experience. Specifically, the fast-food chain intends to use the technology for back-of-house tasks and, starting next year, to deploy new software for its digital platforms.

Restaurants and solution providers alike are also using generative AI to automate the often labor-intensive voice order-taking process, be it at the drive-thru or on the phone. In June, QSR brand Wendy’s began testing Google Cloud’s large language models for taking voice orders at its drive-thrus. Earlier this month, SoundHound announced the acquisition of voice technology company SYNQ3 to speed the development of new generative AI voice ordering capabilities.

As Krishna Gupta, then-interim CEO of Presto, said earlier this year in a conversation with PYMNTS’ Karen Webster, voice AI in drive-thru is progressing rapidly.

“With OpenAI specifically and large language models in particular, our job is to integrate that into our existing product workflow and make things faster, more personalized, and provide capabilities that frankly weren’t there before,” he said. “All those things matter in the drive-thru.”

The technology is also making its way into the restaurant reservations process. Booking Holdings’ OpenTable has added generative AI capabilities, having announced in March the launch of a plug-in for ChatGPT to power restaurant recommendations via the chatbot.

Generative AI also informs how consumers choose where to order. Reports have shown both Uber Delivery and DoorDash testing chatbots this year to provide personalized recommendations and to enhance the ordering process.

Consumers are engaging with these options. The September edition of PYMNTS Intelligence’s “Consumer Inflation Sentiment Report,” titled “Consumers Know What AI Is — Not How It’s Integrated Into Their Daily Lives,” drew from a survey of more than 2,300 U.S. consumers. It found that 58% of participants had received AI-powered recommendations from a food delivery service.

Overall, businesses are looking toward generative AI to boost their performance going forward. According to data cited in the latest installment of PYMNTS’ “Generative AI Tracker®,” “What Generative AI Has in Store for the Retail Industry,” created in collaboration with AI-ID, 78% of business leaders rank generative AI as the most impactful emerging technology over the next three to five years.

Overall, automation is picking up steam, as Jessica Bryan, vice president of marketing at NCR, noted in the October edition of PYMNTS’ “Digital-First Banking Tracker® Series Report,” “The Restaurant of the Future Is Open. Will Diners Bite?”

“In the next decade, we believe that restaurant brands will drive fast-paced growth by owning the experience in new ways,” Bryan said. “… Advances in digital and automation technology can help liberate restaurant staff from manual tasks, which not only makes their jobs easier and more enjoyable but also gives them more quality time to interact with guests.”

CFPB Faces Crucial Supreme Court Decision on Funding in 2024

The Consumer Financial Protection Bureau (CFPB) is reportedly set to face a crucial year in 2024 as the Supreme Court’s decisions loom over its plans to reshape the banking industry’s handling of customer data and fees.

The CFPB, under the leadership of Director Rohit Chopra, has been working on finalizing rules that would make it easier for consumers to share their financial data, switch banks, and have caps on credit card fees, Bloomberg Law reported Wednesday (Dec. 27).

However, the CFPB’s efforts are overshadowed by two key Supreme Court cases that could have a significant impact on the bureau’s future, according to the report.

The first case challenges the CFPB’s independent funding mechanism through the Federal Reserve, while the second case could make it easier to challenge any federal agency’s rules in court, the report said. The court’s rulings in these cases will determine the fate of the CFPB and its rulemaking authority.

One of the cases before the Supreme Court challenges the CFPB’s independent funding mechanism, which currently allows the bureau to request money directly from the Federal Reserve, per the report. The Fifth Circuit Court of Appeals found this funding mechanism to be in violation of the Constitution’s appropriations clause. However, there is speculation that the Supreme Court will not deem the CFPB’s funding unconstitutional.

A ruling in favor of the CFPB would revive its long-awaited rule to restrict payday lenders’ access to customer bank accounts, according to the report.

The Supreme Court’s conservatives could also use a separate case to limit the power of federal regulators by overturning the Chevron deference doctrine, the report said. This doctrine requires judges to defer to expert regulatory agencies’ interpretations of ambiguous statutes. Overturning Chevron deference would open up challenges to many existing regulations, including those issued by the CFPB.

In addition to these legal challenges, the CFPB has been working on implementing rules that would require banks to allow customers to easily transfer their financial data to third-party companies, known as the open banking rule, per the report.

The CFPB also plans to subject the largest digital payments providers and digital wallet operators to direct supervision by agency examiners, according to the report.

The CFPB is also considering new regulations to limit bank fees for overdrafts and insufficient funds, as well as an overhaul of implementing rules for the Fair Credit Reporting Act, the report said.

The Supreme Court is likely to rule on the ways in which the CFPB is funded, as well as the very constitutionality of the agency, during the spring term, PYMNTS reported on Dec. 20.

Nothing Transformative About OpenAI’s Copyright Abuses, Says New York Times Lawsuit

News publisher The New York Times said it owns over 3 million registered, copyrighted works.

On Wednesday (Dec. 27), the NYT sued both Microsoft and OpenAI’s family of operating subsidiaries for violating the bulk of the protections bestowed by them.

“Through Microsoft’s Bing Chat (recently rebranded as ‘Copilot’) and OpenAI’s ChatGPT, defendants seek to free-ride on The Times’s massive investment in its journalism by using it to build substitutive products without permission or payment,” the NYT wrote in its complaint, adding that “the law does not permit the kind of systematic and competitive infringement that defendants have committed.”

“OpenAI quickly became a multibillion-dollar for-profit business built in large part on the unlicensed exploitation of copyrighted works belonging to The Times and others,” the NYT added.

Sophisticated artificial intelligence systems more broadly have upended the applications of existing intellectual property and copyright laws as they have scaled across the marketplace with buzzy, consumer-facing applications meant to capture market share and share of mind.

“I think [the lawsuit is] going to put a shot across the bow of all platforms on how they’ve trained their data, but also on how they flag data that comes out and package data in such a way that that they can compensate the organizations behind the training data,” Shaunt Sarkissian, founder and CEO at AI-ID, an AI tracking, authentication, source validation, and output data management/control platform, told PYMNTS.

“The era of the free ride is over,” he added.

Reached by PYMNTS, an OpenAI spokesperson said the firm respects the rights of content creators and owners and is “committed to working with them to ensure they benefit from AI technology and new revenue models.”

“Our ongoing conversations with The New York Times have been productive and moving forward constructively, so we are surprised and disappointed with this development,” the spokesperson said in an emailed statement. “We’re hopeful that we will find a mutually beneficial way to work together, as we are doing with many other publishers.”

Microsoft did not immediately reply to PYMNTS’ request for comment.

Generative AI and large language models such as ChatGPT gain their wisdom by scraping the web. They use automated software to download countless web pages as well as natural language processing to extract information from web pages built, often at great expense, by others.

In some ways, the problem at hand is as old as the internet itself.

See also: Why Gen AI’s Creative Power Calls for Strategic Oversight

‘Large-Scale’ Content Exploitation

The NYT noted in its lawsuit that the publisher reached out to Microsoft and OpenAI in April to raise intellectual property concerns and explore the possibility of an amicable resolution that would allow a mutually beneficial value exchange, highlighting the NYT’s history of working productively with large technology platforms to permit the use of its content in new digital products, including the news products developed by Google, Meta and Apple.

But nothing came of those entreaties.

“As part of training the GPT models, Microsoft and OpenAI collaborated to develop a complex, bespoke supercomputing system to house and reproduce copies of the training dataset, including copies of The Times-owned content. Millions of Times works were copied and ingested — multiple times — for the purpose of ‘training’ defendants’ GPT models,” the NYT lawsuit stated.

While Microsoft and OpenAI have in the past insisted that their conduct is protected as “fair use,” the NYT complaint disabused the notion that the “use of copyrighted content to train GenAI models serves a new ‘transformative’ purpose.”

“Because the outputs of Defendants’ GenAI models compete with and closely mimic the inputs used to train them, copying Times works for that purpose is not fair use,” the complaint stated.

An analysis by The Washington Post in April of just one dataset used for training AI found that nearly the entire 30-year history of the internet has been scraped by tech companies looking to add to the billions, even trillions, of parameters their models are trained on.

The complaint pointed specifically to the Common Crawl dataset, which was the most highly weighted training dataset for OpenAI’s GPT-3, noting that the domain www.nytimes.com is the most highly represented proprietary source in the set.

Other news publications whose content featured prominently in the dataset include The Guardian, The Los Angeles Times, Forbes and the Huffington Post.

Read also: Google and Microsoft Spar Over Training Rights to AI Data

The Future of Publishing Is Inextricably Intertwined With AI

The suit from the NYT comes amid several other court cases involving AI. For example, the summer saw at least two lawsuits from groups of writers against OpenAI, accusing the company of training its AI with copyrighted works without their permission, and of using illegal copies of their books pulled from the internet.

Some publishers have, as the NYT tried to without success, reached commercial agreements to license their content to OpenAI, including the Associated Press and Axel Springer.

The U.S. Copyright Office has launched an initiative to study the use of copyrighted materials in AI training, indicating that legislative or regulatory steps may be necessary in the near term to address the use of copyrighted materials within AI model training datasets.

“What this case will likely do is create a benchmark of what is the economic threshold, or what are reasonable royalties, for fair use of content,” Sarkissian said. “Everyone’s going to use The New York Times as a proxy and see how it goes.”

The lawsuit requests a trial by jury but does not make a specific monetary demand. The complaint does, however, emphasize that Microsoft and OpenAI should be held responsible for “billions of dollars in statutory and actual damages.”

“If The Times and other news organizations cannot produce and protect their independent journalism, there will be a vacuum that no computer or artificial intelligence can fill,” the lawsuit stated.

Apple Wins Legal Victory as Court Lifts Watch Ban

Apple can resume selling its latest smartwatches in spite of a recent import ban.

A federal appeals court on Wednesday (Dec. 27) paused that ban, CNBC reported, allowing the tech giant to once again sell its Series 9 and Ultra 2 watches.

The ban went into place last week following a ruling by the International Trade Commission (ITC) order that found the blood oxygen sensor in the devices had infringed on intellectual property from medical technology firm Masimo.

“The motion for an interim stay is granted to the extent that the Remedial Orders are temporarily stayed,” a court filing Wednesday said, per CNBC.

Masimo had sued Apple in 2020, claiming the company had stolen trade secrets associated with health monitoring technology and poached important staff members.

Following the ITC’s initial ruling in October, Apple said that Masimo had “wrongly attempted to use the ITC to keep a potentially life-saving product from millions of U.S. consumers while making way for their own watch that copies Apple.”

Apple had appealed that ruling, but the ITC last week denied that request, thus halting imports and future sales of the newest watches. Previously imported Apple Watches can be sold if retailers still have them in stock. The ban also does not affect older versions of the watch, which do not include the disputed blood-oxygen sensor.

With the ITC refusing to lift the ban, Apple had hoped for the White House to overrule the agency. However, the administration — personified here by the U.S. Trade Representative — declined to intervene earlier this week.

The CNBC report notes that Apple Watch sales are part of the company’s wearables business, which recorded $39.8 billion in sales in Apple’s fiscal 2023.

That coincides with a growing interest — and use of — among consumers in connected devices that monitor the “progress of everything, from the number of steps walked to vital signs to reminders about prescriptions,” PYMNTS wrote earlier this year.

Research has found that a large percentage of consumers use digital channels to track their health data on both a daily (26%) and weekly basis (11%).