In this article, we will look at the SVB Meltdown and see if this is just a nothing burger or a part of an underlying systemic issue created by the central banks.

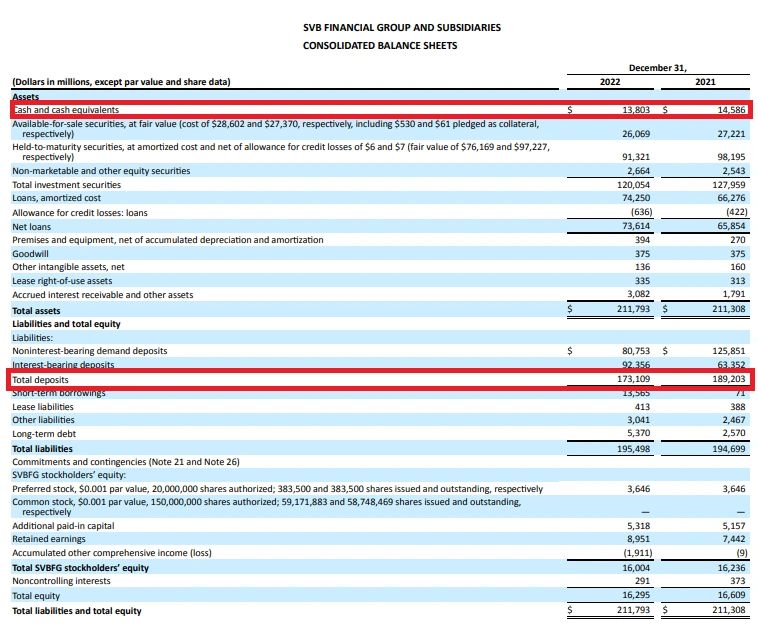

So we’ve all heard that Silicone Valley Bank has failed, and it’s put into FDIC receivership. The FDIC holds about $129B in assets in their insurance fund. SVB, as per their December 2022, held $173B on their balance sheet. The issues started with a bank run where they had to sell their treasuries to cover asset flight from bank deposits. The problem is that the treasuries are being sold at a loss due to rising bond rates. Most likely, Bailins are coming to SVB.

SVB Stock is down 60% overnight.

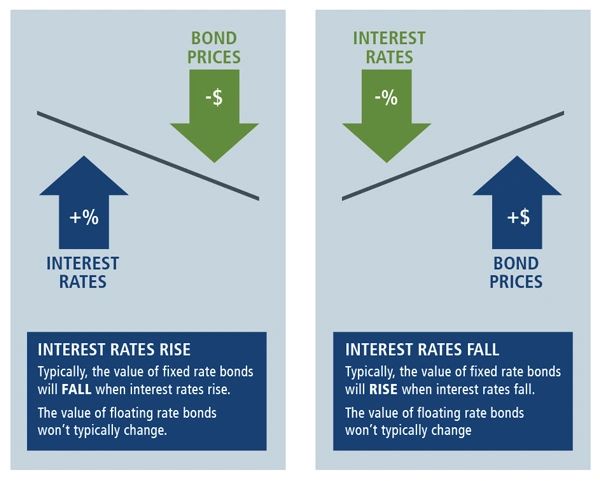

How bonds lose value:

So showing the above, SVB had an influx of deposits during covid from PPP and other cash stimulus programs from the US Treasury. When SVB got a deposit, they needed a bond to cover as an asset to the deposit liability on the bank balance sheet. What happened was that interest rates rose from when they had bought the term bonds, and the value, as explained above, had fallen on their bonds. So when the deposit exodus started, they had to sell their bonds and get a lesser value back than what they paid. What this does is that when the depositors move away, they have to sell their bonds and then give the bank reserve, which is the bank that had the deposit transfer “cash.” Now with a loss in the value of bonds, they want to have enough cash to cover the transfer to another bank.

That is the digital deposit transfer. Their Cash and Equivalents are only at $13.8B, so if the deposits didn’t digitally transfer hands and people wanted cash, only 7.98% of depositors would withdraw cash, and it would go bankrupt. The reality is that cash and equivalents are not cash only. It’s also digital deposits at other banks. This means that a physical cash withdrawal would probably collapse the bank at a 2% or even less physical cash withdrawal rate.

When this happens to banks like JPMorgan, Goldman Sachs, Wells Fargo, Citibank and other banks in the US that have access to reserve accounts at the Federal Reserve, they would have their assets bought by Quantitative Easing by the FED, creating reserves in the Banks FED account and taking their bad assets like MBS and Treasuries and leaving them on their balance sheets.

.jpg/:/cr=t:0%25,l:0%25,w:100%25,h:100%25/rs=w:1280)

Looking at the chart above, you can see that many banks have fewer FDIC-insured assets. Still, my worry is the bigger banks with an insane amount of assets under $250k will be pretty insane. The FDIC is a minnow about to get eaten by a shark when even a bottom 20 bank fails. Also, deposits other banks had with SVB can cause massive contagion and many investment banks and fund-owned shares in SVB. Many Venture Capitalists from Silicon Valley had deposited there and are now crying. They want all their assets back from the bank. They had no clue they could fail!

Thousands of banks have failed throughout history, and this will not be the last, as it seems the crash and collapse have barely started!

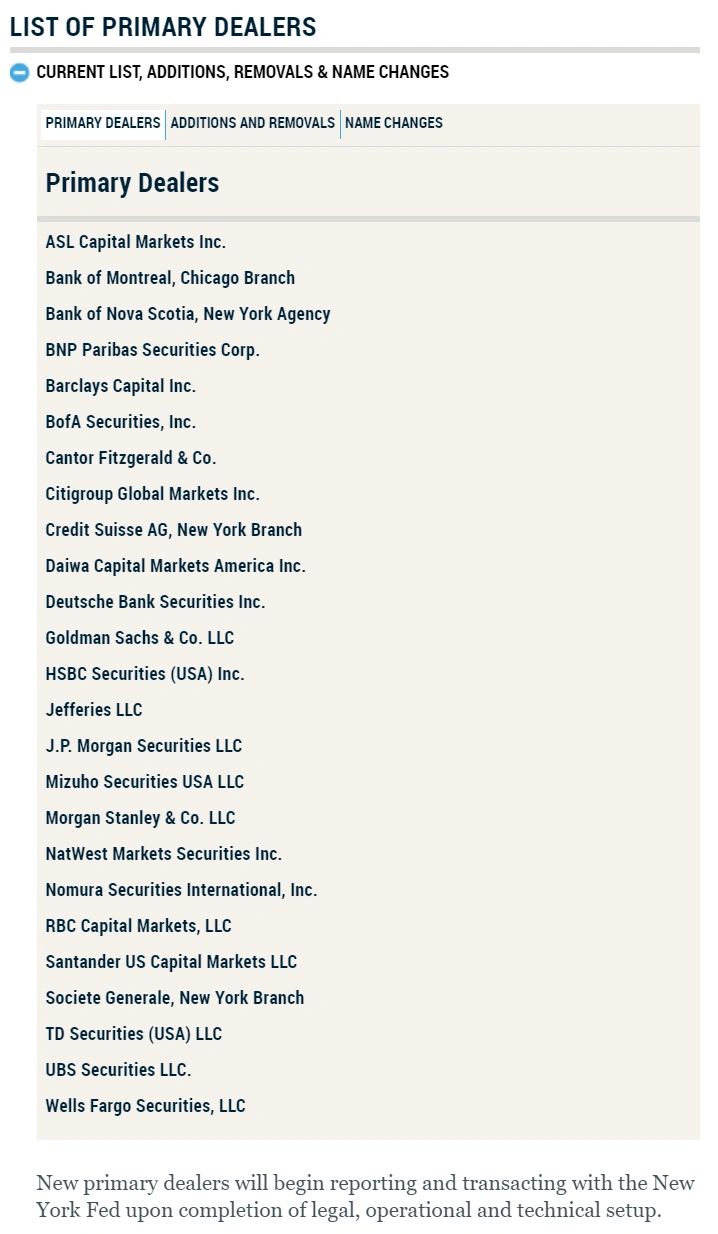

Here is the list of banks that would be bailed out overnight by the US Central Bank. Here you can find the banks that will get bailed out when the above happens!

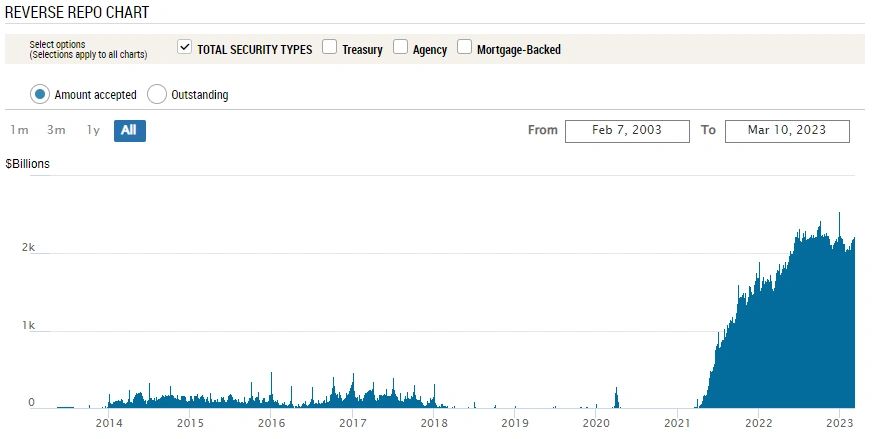

Most banks listed above don’t even care about depositors as they can have money sitting at the Federal Reserve overnight at the current 4.55%. There are currently, as of today, 100 institutions doing this. This is called Reverse REPO, and the list is extended to GSE Government Sponsored Entities, ETFs and Money Market Funds. Currently, the 100 Entities that are using this hold $2.188T. Before 2008 this market manipulation wanted to be used or exist. No actual economic activity is created by sitting in this account, and it is highly destructive for our society!

Let’s get back to the losses that SVB has faced. Is only Silicon Valley Bank having this issue, or is it a massive contagion about to happen? A recent post from the FDIC gives a little context to this issue, and it’s not only banks facing losses like this. It is the Central Banks themselves! Here is the FDIC’s article and chart that shows the bank’s Unrealized Gains or Losses.

How about the central banks?

As of the third quarter of 2022, the Bank of Canada had lost CAD 522M. The FED, as per Q3, was down about $720B on their portfolio. Bank of England is down £200B. Hungary’s Central bank has lost about 200B Hungarian Forints. The Swiss National Bank has lost about 18% of the Swiss GDP at $143B Swiss Francs. These are just examples of a few central banks that did what SVB did. Buy bonds when they are low, but not sell them. What the FED and others have done is instead of selling them at a loss, they are just letting the bonds run out as they are the ones owning them and don’t care about losses. The reason is that they can create a supply out of thin air to buy these assets. The problem becomes their long portfolio of 20Y,30Y or longer bonds.

Now that we’ve seen the cause of loss from government debt let’s look at losses caused by consumer and corporate debt and private debt.

In banking, debt is an asset. A Deposit is a liability. The bank’s reasoning for being an asset is that it is technically prudent and protects itself against a drop in an “assets” price. For example, a house the bank would lend you 80% of the purchase value of your home, and you will have to put up 20% of the home’s value. The bank now has a loan-to-value on your home, sitting at 80% loan-to-value. So even if the home dropped 20%, the bank would still be 100% loans to value, and it’s an asset. The debt is still worth the same as the value of the home. The problem came when people borrowed cash from places that gave them more debt to the house’s value. After 20%, banks will start to have an issue as people’s homes value would drop below what they owe on the home. Let’s say the home’s value collapsed down 40%. Now the loan to value would be 125%. So if the bank’s loan was $80k, the house value was $100k and dropped to 60%, the new loan to value is 133.33% or what banks call negative equity.

When this happens, many people see no hope in their future to pay their mortgage and might walk away and declare bankruptcy. This will hurt the bank, and if enough people do this, the bank might have insane losses on its balance sheet. It will most likely get a bailout if they have a seat on the Federal Reserve Primary Dealer list and will have that debt purchased. Now that debts aren’t directly purchased, banks issue derivatives on top of that debt, mostly in mortgage terms called Mortgage Backed Securities. A GSE like Fannie Mae or Freddie Mac insures many mortgages. The FED will buy the MBS from these institutions to prevent the insurer from collapsing. An MBS is 1000’s mortgages packaged together in a corporation, an LLC called a Special Purpose Vehicle, used by banks to hide their assets off their balance sheets to look better.

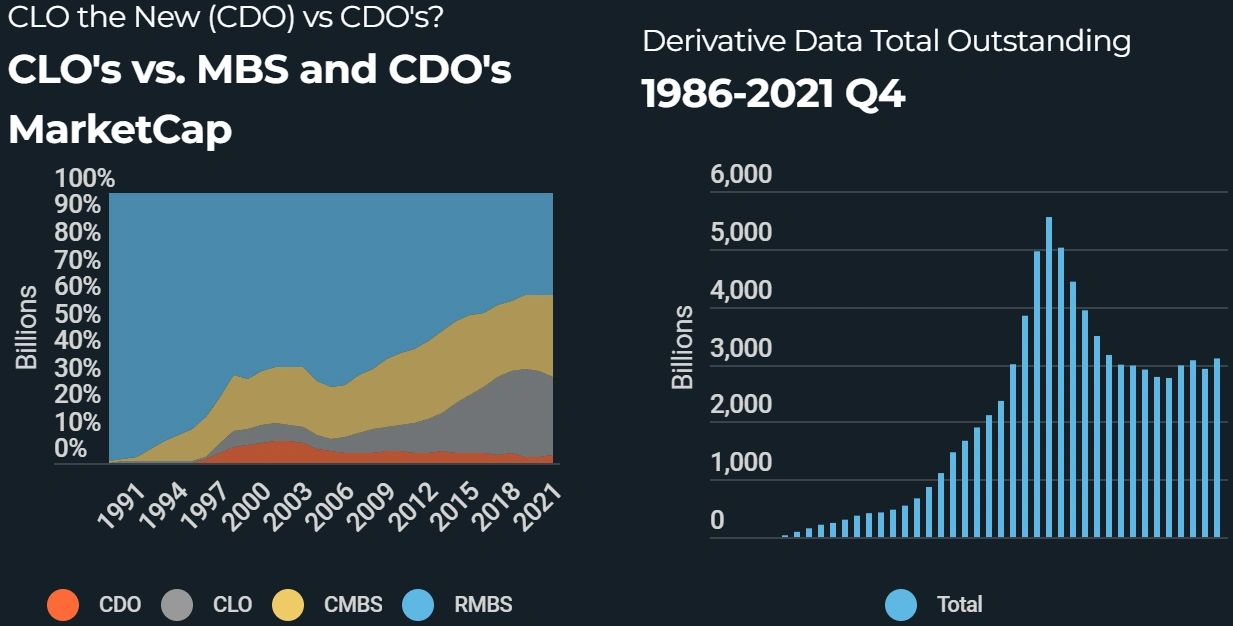

Now, that’s housing. The same could happen to cars it will happen to cars, but lenders hope that the loans on cars keep track of the value of the car. If demand for cars collapses, the value of the car purchased when demand was high could drop faster than the debt owed to the bank, and if the person cannot afford this debt due to he lost his job or the person sees selling his car as useless that person could give up and walk away. The car then gets repossessed by the bank, and they try to sell it, but if there is no demand, the bank faces losses. As with MBS, there is another derivative for this type of consumer debt called Asset-Backed Securities. Now in this class, there is secured and unsecured debt. A car, camper, boat or motorcycle would be an example of secured debt as an “asset” exists. Unsecured debt is a personal line of credit not attached to the value of a home or the mentioned consumer credit card. But all of this debt gets packaged the same way and collapse similarly. Then there is corporate debt and corporate real estate. They are similar to consumer debt but are called CMBS, CRE CLO or CLO. Commercial Mortgage Backed Securities, Commercial Real Estate Collateralized Loan Obligation or Collateralized Loan Obligation. The latter is corporate debt. The two first is real estate debt.

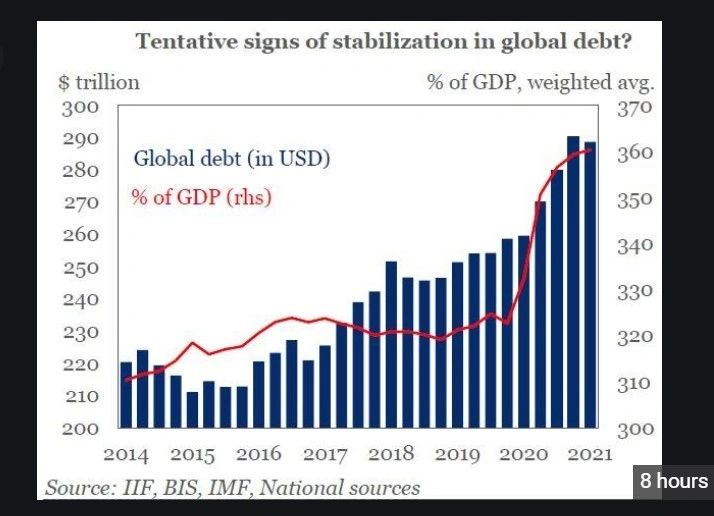

So that said, rising debt levels of all kinds and interest rates mean the cost of servicing this debt will skyrocket. This means their savings and income will get eaten up, and their possibility to buy things will dwindle. Viola demand shrinks, layoffs happen, defaults on debt happen, and we have a recession or depression.

But the reaction to this since 2008 has been the solution of central banks, by creating reserves and buying assets—derivatives off the bank’s balance sheet to save them.

Derivatives are smaller than in 2008. But what has happened is that corporate derivatives have taken over private derivatives as a part of the economy.

When derivatives fail or debt defaults, we have a new but old kid called a CDS, Credit Default Swap. They are insurance policies, but it doesn’t have insurance in their name because Blythe Masters, the inventor, didn’t want them to be governed under insurance legislation which is a lot stricter than the derivative world. But don’t be fooled. It is an insurance policy, but 100 or 1000s can insure the same thing instead of individual insurance. In simple terms, your house would be insured by 1000 people, and when your house burns down, not the person who owns the asset gets paid but 1000s that don’t even own the asset. This is why AIG, the world’s biggest insurer, failed in 2008 and got bailed out.

So with all the derivatives, if the underlying debt fails, that might not be the most significant trigger. The insurance on the fake asset could be the massive trigger!

My last thoughts are that governments worldwide will react by “printing” currency through direct “cash” injections through helicopters, bombers or even monetary nukes to stop the deflation of debt from taking hold and destroy the monetary Ponzi scheme we have on a global scale now. Like Ben Shalom Bernanke described in his 2002 FED speech Deflation: Making Sure “It” Doesn’t Happen Here. “The Printing Presses always win over deflationary pressures.” He also described that the FED might have to buy a more comprehensive array of assets. Other central banks like the Japanese, European, Chinese and Norwegian central banks did this by buying commercial real estate, corporate debt, stocks and other government debt.

So we are in a global debt bubble in all private, corporate and public sectors. We have a global Ponzi scheme that is only held together by the glue of trust in its value. When that break, so will our current monetary structure! We’ll all end up like poor serfs on the monetary plantation if we don’t get off the monetary grid!